Most insurance policies cover unexpected travel disruptions like medical emergencies, lost luggage and flight delays

Losses from common travel scams are usually excluded, but some policies may cover these

Whether a scam is covered or not may depend on whether the insurer considers it a ‘cyber incident’

Here at CHOICE, we consider travel insurance to be an essential part of planning a holiday, especially if you’re leaving Australia.

This is because if things go wrong, you could end up paying big bucks to get your holiday back on track and travel insurance policies can help cover these costs.

Most people get travel insurance in case they need medical treatment overseas – you’re unlikely to get the same subsidised arrangement as in Australia, so foreign medical bills can escalate into the hundreds of thousands of dollars.

Depending on the level of cover you choose, travel policies can also help smooth over transport cancellations, delays, lost luggage and even cover costs stemming from seismic events like natural disasters and pandemics.

Are scams covered?

Australians lost almost $260 million to scams this year and the stories we’ve heard from consumers confirm cons targeting holiday makers have contributed to that toll.

Online scams like fake accommodation listings and hacked hotel profiles have led to consumers losing hundreds of dollars in one fell swoop.

Meanwhile, more traditional schemes like being overcharged for a taxi or tickets can also still knock a hefty hole in your holiday budget.

So will travel insurance cover you for these losses? We dive into the fine print to find out.

Travel insurance providers have to explain what they will and won’t cover in each policy’s product disclosure statement (PDS).

We looked through 89 of these documents, detailing the ins and outs of multiple policies from some of the most well-known providers, and reached out to several insurers directly to ask if they would cover losses stemming from common travel scams.

In bad news for scam victims, most policies don’t cover losses from scams, fraud or other situations where people have abused your confidence, tricked or deceived you.

In bad news for victims, most policies don’t cover losses from scams

“Broadly, the only travel insurance cover for scams or fraud is in relation to if your credit card is lost or stolen while overseas, and then used fraudulently,” says CHOICE insurance expert Jodi Bird.

“And only a few policies appear to cover you if your credit card details are skimmed or stolen, as opposed to the card itself being taken.”

But one insurer we looked at considers several common travel scams “cyber incidents” and does provide cover for policy holders in these situations.

To pinpoint where these differences in cover emerged, we looked at how insurers would respond to five common travel scam scenarios.

CHOICE tip: Your travel insurance provider may not cover scam losses, but may be able to help you take steps to protect yourself after you’ve been scammed, such as filing a police report and canceling bank cards.

1. Fake accommodation listing

Criminals have been known to set up scam listings on holiday accommodation and rental sites.

Picture it: you’ve snagged a great price for a fetching property listed on an established short-stay platform like Booking.com or Airbnb.

But on arrival, you discover the property doesn’t exist and the money you sent the host to secure the booking has disappeared.

Jodi’s interpretation of a raft of policies from across the market suggests not.

“Many policies contain an exclusion that relates to a ‘cyber act’,” he explains.

“Cyber acts can be a threat or hoax threat involving access to, processing of, use of or operation of a computer system. This definition likely excludes cover for an accommodation listing ‘hoax’.”

We heard a similar story when we presented this scenario to the insurers we contacted.

Travel policy provider Go Insurance confirmed they didn’t cover customers for losses caused by fake listings because they excluded fraud and deception.

At least one insurer, however, does promise to cover policy holders who lose money to a fake listing scam – Passport Card told us it considers this scenario a “cyber incident” and said it would cover for the disruptions it would cause.

Hackers can take over accommodation accounts on booking platforms and message guests. Image: WA ScamNet

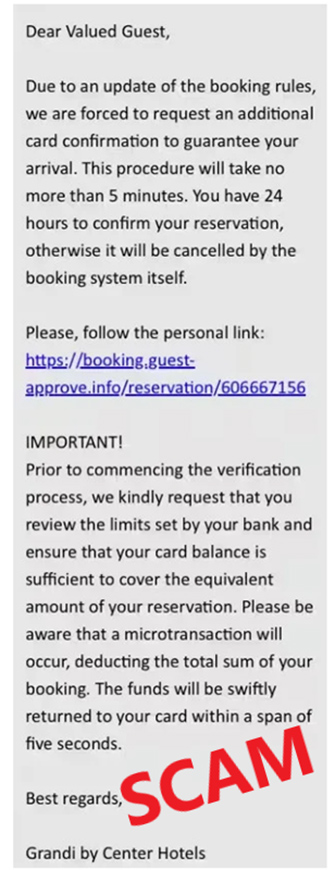

Another scam known to occur on major booking platforms involves hackers taking control of an accommodation provider’s account and using it to message guests.

Customers who have booked to stay at the affected property will receive messages appearing to come from the provider asking them to make extra payments (into an account controlled by the hackers) to secure their reservation.

Jodi says losses to this type of scam also won’t be covered by most travel policies.

“Travel insurance primarily covers events that occur when you are already on a trip, so presuming you sent the money before your departure, it won’t be covered,” he says.

“And if you made such a booking on a trip, it would probably be excluded by a ‘cyber act’ clause.”

But again, there are some differences between individual insurers here.

Most insurers don’t cover for this type of scam, but Passport Card said they would also consider this event to be a cyber incident and will cover it.

Preparing for a trip overseas often involves going online to obtain important documents like visas, transport tickets or driving permits ahead of your departure.

Unfortunately, dodgy websites promising to source these are a threat to be reckoned with and can appear among search engine results.

Visitors to these pages might be charged high fees for documents that are fake, overpriced or never provided at all.

Unfortunately, most travel insurance policies won’t reimburse money you’ve sent away before your trip for a visa that didn’t arrive

“Travel insurance primarily covers events that occur when you’re already on a trip, so presuming the booking was made at home, before your departure, it won’t be covered,” Jodi explains.

In this instance, all the individual insurers we reached out to were in lockstep in not providing cover for this situation.

Read more:

4. Taxi overcharging

More than a few of us have been there – arriving in a foreign city, you take a ride with a taxi driver who overcharges you for the journey.

Our assessment of PDS documents didn’t unearth any specific clause excluding this.

One insurer, however, did exclude “Any scam or fraud that you could have reasonably anticipated or avoided”.

“This is an obvious grey area,” notes Jodi. “If you could have ‘reasonably anticipated or avoided’ a scam, surely you wouldn’t have got scammed to start with.”

In any case, the insurers we presented the taxi scam scenario to said they wouldn’t cover it.

A perennial travel scam, pickpocketing is fortunately covered by most travel insurance policies.

Not a scam per se, but grabbing something valuable from right under your nose is the ultimate goal of criminals in some locations who may target backpacks or pockets that are easy to reach without you noticing.

In some cases the criminals will orchestrate distractions by pretending to be beggars or charity fundraisers in order to gain access to your valuables.

Luckily, this is the type of “physical loss” that travel insurance is likely to cover.

“Just ensure you get a police report to give to your insurance provider,” Jodi advises.

Ultimately, most travel insurance policies are designed to tackle truly unexpected disruptions like medical emergencies, cancelled flights or natural disasters.

Most insurance policies don’t cover for scams, but some providers like Passport Card may reimburse you if you fall victim to some common travel cons, which it considers to be cyber incidents.

Overall, prevention is better than (no) cure. One of the providers we looked at, Go Insurance, told us:

“Travel insurance is designed to respond to unexpected and disruptive events [but] … scam losses usually sit outside that framework because there’s no insured event for the policy to respond to.”

“It’s the result of deliberate deception rather than something unforeseen happening to your trip. The best protection is still prevention. A few extra checks upfront can save a lot of disappointment once you’re overseas.”

For tips on choosing the best travel insurance to suit your needs, visit our buying guide. For tips on how to spot common travel cons, see our guide on travel scams to avoid.

Liam Kennedy is a Journalist with the Editorial and investigations team. He answers consumers' most burning questions, from which scams to be aware of and how to save money, to whether new services and products are worth using and how the latest developments in consumer news could affect them.

Prior to CHOICE, Liam worked in production in daily news radio and podcasting.

Liam has a Bachelor of Communication (Journalism) and a Bachelor of Arts in International Studies from the University of Technology Sydney. LinkedIn

Liam Kennedy is a Journalist with the Editorial and investigations team. He answers consumers' most burning questions, from which scams to be aware of and how to save money, to whether new services and products are worth using and how the latest developments in consumer news could affect them.

Prior to CHOICE, Liam worked in production in daily news radio and podcasting.

Liam has a Bachelor of Communication (Journalism) and a Bachelor of Arts in International Studies from the University of Technology Sydney. LinkedIn

For more than 60 years, CHOICE has been fighting the good fight for Australian consumers.

In the past year alone we've uncovered systemic issues with sunscreens, investigated shonky supermarket pricing, fought for stronger scam protections and helped make complex energy pricing fairer and clearer.

CHOICE is here to provide unbiased advice and independent testing in our world-class labs. We buy the products we test, just like you do, and our expert reviews are influence free. We’re here to help you choose smarter. Hopefully you’ll also save some money along the way.

Thanks to CHOICE, you’ll never be alone when a business treats you unfairly. You can support our work by joining or donating to our cause.