Flights have resumed through the major Middle East air transit hubs, but Smartraveller still advises you to avoid non-essential travel through much of the region as the situation there remains volatile.

So should you still plan travel through the region, and what do you do if your trip is interrupted by war? Will your travel insurer help you?

Most travel insurers in the CHOICE travel insurance comparison exclude cover for claims that arise as a result of war. This includes flights interrupted by military strikes in the Middle East.

Travel insurers specify this in the General Exclusions section of their Product Disclosure Statement. It is generally stated as:

We will not pay for claims arising as a result of war, invasion, act of foreign enemy, hostilities (whether war be declared or not), civil war, rebellion, revolution, insurrection or military or usurped power.

CHOICE tip: Go Insurance is the only brand in the CHOICE travel insurance comparison that provides some cover for claims resulting from war. Its policies cover medical expenses and repatriation for wars that happen after you’ve already departed home – so it doesn’t cover the current war in the Middle East. For an additional cost, limited cover is also available for additional expenses to re-arrrange your trip.

Does travel insurance cover trips interrupted by government travel warnings?

Australian government travel warnings can affect your travel insurance cover, depending on the specific travel advice.

DFAT’s Smartraveller website assigns destinations an official advice level of 1, 2, 3 or 4. A higher travel advice level means higher risk. The levels are:

Level 1 (Green) – Exercise normal safety precautions

Level 2 (Yellow) – Exercise a high degree of caution

Level 3 (Orange) – Reconsider your need to travel

Level 4 (Red) – Do not travel

Travel insurance will not cover claims arising from travel to a destination that has an Australian Government “Do not travel” warning.

Some travel insurers may cover you to travel to destinations covered by a “Reconsider your need to travel” warning, but many don’t, so you need to check the fine print of your travel insurance policy.

If the warning level for your destination was escalated, for example from Level 1 “Exercise normal safety precautions” to Level 4 “Do not travel”, after you bought your policy, travel insurers may cover you to change plans, but only if the reason for the claim isn’t already excluded by the insurer.

Since claims due to war are generally not covered by travel insurance, you will still not be covered for claims due to war.

CHOICE tip: You should still contact your travel insurer and lodge a claim. If you’re stranded due to a cancelled flight, tell your insurer your flight was cancelled due to “airspace closure” (i.e. don’t mention the war), and let the insurer decide if your claim will be covered.

What will your travel insurer help with?

If your claim isn’t related to war, you may be covered for other incidents. You may also have some cover in a ‘Do not travel’ destination if you bought your policy before that advice was published.

For example, if you are unable to change your plans and your flight or tour transits through a destination with a Smartraveller “Do not travel” advice, you may be covered if you break your toe on the stairs. But if your hotel is bombed in a drone strike, you may not be covered.

Insurers may also offer you a free extension of your insurance if you bought your travel insurance policy before a travel advice was escalated to “Do not travel”.

If your claim isn’t related to war, you may be covered for other incidents

So if you’re stranded overseas for longer than you planned, speak to your insurer about extending your policy. That way you’ll at least still have cover for events unrelated to the military conflict, such as if your phone is stolen or you slip in the shower and need medical attention.

Insurers should also offer support via their emergency assistance, for example to help you coordinate medical care, access prescription medication or to report an incident you want to claim for.

What should you do if your flight is booked through the Middle East?

Keep an eye on your airline’s advice about your flight, especially if you have a stopover in the Middle East.

If you cancel your ticket you will be subject to the terms and conditions of the ticket. Unless you have a flexible ticket, you’re unlikely to get your money back from the airline. However, if the airline cancels the flight, you will usually be entitled to a refund or credit.

If the airline cancels the flight, you will usually be entitled to a refund or credit

If the airline has cancelled or delayed flights due to war or a “Do not travel” warning, it’s considered an event that is out of their control and the airline will have a policy providing compensation for compensation for cancellation or delay. Familiarise yourself with the policy in case you need to remind the airline of their terms and conditions, because they won’t necessarily volunteer it to you.

Let your airline know if you’re unable to get to the airport due to a war. If you can get a real person on the phone who you can explain your situation to, that will help, otherwise try the airline’s social media accounts. That will often get a response where other avenues don’t.

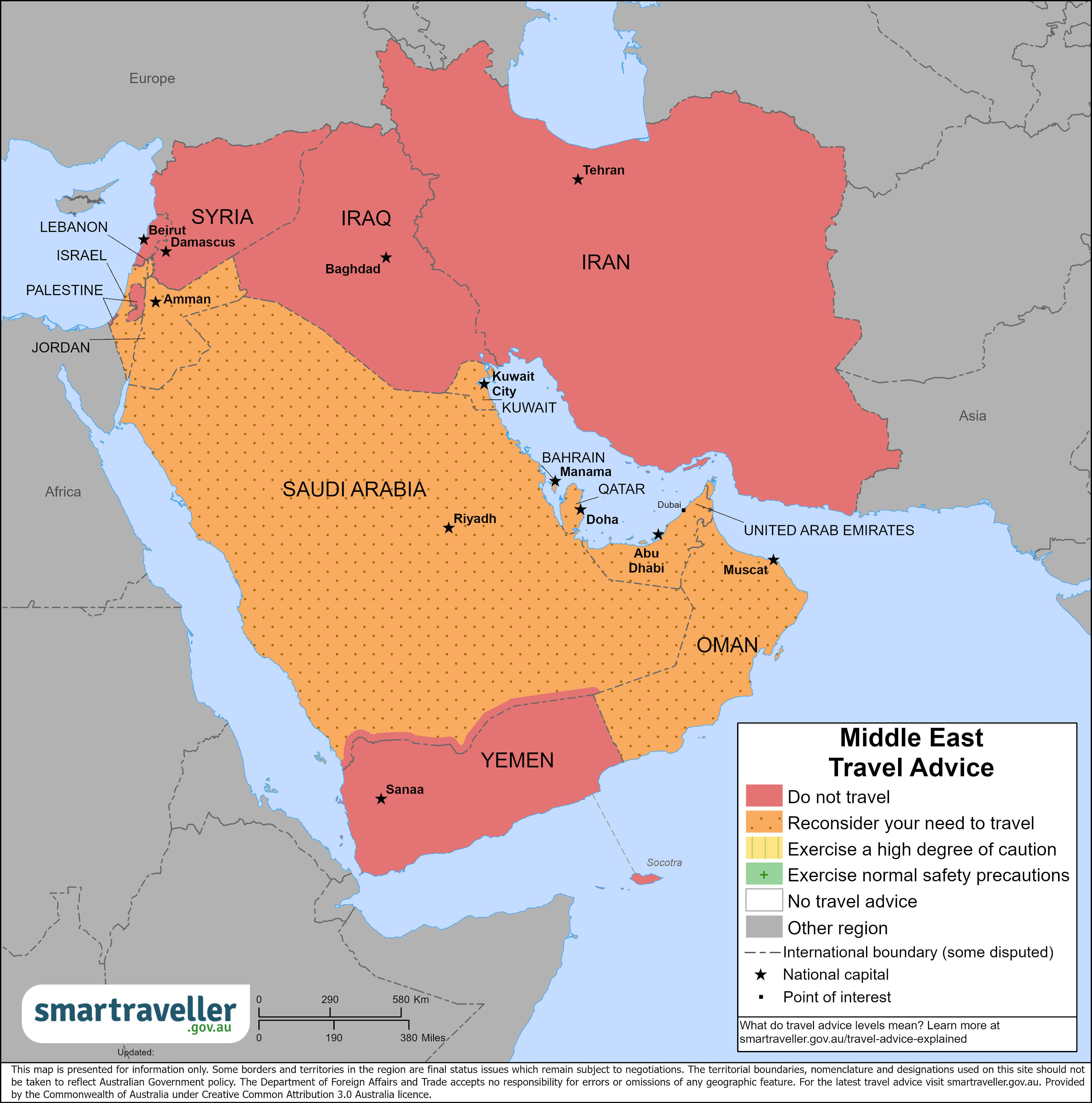

The Smartraveller advice is currently set to “Reconsider your need to travel” or “Do not travel” for the Middle East. The travel advice applies to stopovers in the destination as well as longer stays.

Transit hubs such as UAE and Qatar are at Level 3 “Reconsider your need to travel”. Smartraveller advises you to avoid non-essential travel to these locations. If you need to transit, stay as short a time as possible. You should also read your travel insurance policy to understand if it covers destinations with “Reconsider your need to travel” travel warnings.

How to get money back on accommodation

Keep an eye on your airline’s advice because your airline may cover accommodation costs incurred due to flights cancelled or rescheduled due to the military conflict.

Otherwise, contact your accommodation provider and ask if you can reschedule or get a refund. Military situations have a big economic impact on tourist destinations, so flexibility on both sides of the equation can help the community, as well as ensuring you still get a holiday.

How to get money back from third-party booking sites

Booking sites generally have their own terms and conditions, so if you booked through them, you should deal with the booking site, not the end-point service provider. The booking site should still be subject to Australian Consumer Law.

The sites usually have standard cancellation policies, but in the event of war, they may make an exception. Airbnb, for example, may waive cancellation penalties in the event of a war. So familiarise yourself with the booking site’s policy and quote it to them if necessary.

You’ve tried everything else, is there any other way to get your money back?

When you have exhausted your attempts to get money or a credit back from your airline, accommodation or travel agent, you should still lodge a claim with your travel insurer – even if you don’t think you’ll be covered.

If you don’t think you got a fair go from your travel providers, then you may also want to consider raising a credit card chargeback.

Jodi Bird is the Managing Financial Content Editor at CHOICE. Previously at CHOICE, he worked as Travel project lead and as a Finance specialist.

Jodi has extensive experience in financial services, having worked with major banks such as CBA, Westpac and Credit Suisse. He enjoys breaking down complex consumer decisions into easy to understand steps and holding companies to account for failing their customers. He is regularly called upon for expert commentary by major broadcasters such as the ABC, SBS, and Channels 7, 9, and 10.

Jodi has a Bachelor of Commerce majoring in Economics from the University of Wollongong. He is RG146 compliance certified to provide general advice for General Insurance and is a Responsible Manager on CHOICE's Australian Financial Services License. LinkedIn

Jodi Bird is the Managing Financial Content Editor at CHOICE. Previously at CHOICE, he worked as Travel project lead and as a Finance specialist.

Jodi has extensive experience in financial services, having worked with major banks such as CBA, Westpac and Credit Suisse. He enjoys breaking down complex consumer decisions into easy to understand steps and holding companies to account for failing their customers. He is regularly called upon for expert commentary by major broadcasters such as the ABC, SBS, and Channels 7, 9, and 10.

Jodi has a Bachelor of Commerce majoring in Economics from the University of Wollongong. He is RG146 compliance certified to provide general advice for General Insurance and is a Responsible Manager on CHOICE's Australian Financial Services License. LinkedIn

For more than 60 years, CHOICE has been fighting the good fight for Australian consumers.

In the past year alone we've uncovered systemic issues with sunscreens, investigated shonky supermarket pricing, fought for stronger scam protections and helped make complex energy pricing fairer and clearer.

CHOICE is here to provide unbiased advice and independent testing in our world-class labs. We buy the products we test, just like you do, and our expert reviews are influence free. We’re here to help you choose smarter. Hopefully you’ll also save some money along the way.

Thanks to CHOICE, you’ll never be alone when a business treats you unfairly. You can support our work by joining or donating to our cause.