Card schemes such as Visa or Mastercard govern the chargeback process and each one has their own rules for when you can get a chargeback

Banks and credit unions are legally obliged to pursue a chargeback on your behalf if you have a right to one under your card scheme’s rules

There are time limits on disputing transactions. If you miss the deadline, you’re likely to miss out on getting your money back

If there’s something wrong with an item you’ve bought with a credit or debit card, you may be able to get a refund by asking your bank or credit union for a chargeback. A chargeback reverses a transaction, refunding the money you paid for a product or service.

You can also get a chargeback for incorrect or fraudulent transactions made on your account.

Before requesting a chargeback

Contacting the retailer directly if there’s a problem is often the simplest and quickest way to get a remedy.

In any case, Visa expects you to try to resolve the issue with your retailer before asking for a chargeback. In fact, it won’t consider some chargeback requests, such as for an item not received, if you haven’t taken this step.

Mastercard strongly encourages its customers to contact the retailer for a solution before resorting to a chargeback.

You don’t have to accept an alternative offer if you’re entitled to a refund under Australian Consumer Law or the terms and conditions of your purchase

Ask your retailer for a refund or, if you like, an alternative such as a credit voucher or a rescheduled booking. You don’t have to accept an alternative offer if you’re entitled to a refund under Australian Consumer Law or the terms and conditions of your purchase.

If you need to request a chargeback later on, it’s likely you’ll have to prove you tried to resolve the issue with the retailer first, so it’s best to make any requests to the retailer in writing or follow up phone calls with an email.

How the chargeback process works

Banks and credit unions give out credit and debit cards, but a card’s payment system is operated by a card scheme such as Visa or Mastercard.

These schemes govern the chargeback process and each one has their own rules for when a customer can get a chargeback.

If you ask your bank or credit union for a chargeback, they must review your request and decide whether it’s valid, based on the rules of your card scheme, the terms and conditions of your purchase and any relevant regulations.

When you can get a chargeback

Banks and credit unions are legally obliged to pursue a chargeback on your behalf if you have a right to one under your card scheme’s rules.

You will need to give your bank or credit union details about the transaction you’re disputing, your reason for requesting a chargeback, and evidence to back it up such as contracts, invoices and correspondence with the retailer.

Common reasons people ask for chargebacks include:

The item wasn’t supplied by the retailer at all or within the agreed timeframe, including when this happens because of government restrictions or insolvency.

The item is not as described.

There are duplicate transactions (ie, you were charged more than once for the same product or service).

You were charged the wrong amount.

You don’t recognise the transaction.

You cancelled a recurring direct debit but were still charged.

You returned a product or cancelled a service and were promised a refund but never received it.

According to a Mastercard document on disputes during COVID-19, if you’ve bought a travel package through a travel agent that includes multiple services such as flights, hotel accommodation and a cruise, but one of these services is cancelled, you generally have the right to a chargeback for the entire travel package.

Banks and card schemes should be much more clear with customers about what their [chargeback] rights are

Gerard Brody, Consumer Action Law Centre CEO

But you may only be entitled to a partial chargeback if the terms and conditions of the travel package, provided they were shown to you when you bought it, say so.

The retailer you buy an item from – in this example, the travel agent – is responsible for the transaction and will pay the chargeback, if it’s successful.

If your bank or credit union decides your chargeback request is valid, they notify the retailer’s bank. The retailer’s bank may then accept the chargeback and refund your money – or reject it if they decide the chargeback is invalid.

If the retailer’s bank rejects the chargeback and your bank or credit union disagrees with the reasoning, they may ask the credit card scheme to decide.

When you might not get a chargeback

If a retailer has provided a service but you can’t or don’t want to use it, you’re unlikely to be eligible for a chargeback under card scheme rules.

This includes situations where you don’t want to catch a flight or attend an event because of COVID-19 – unless the retailer’s cancellation policy states it’s refundable in such circumstances.

Mastercard and Visa say you can’t get a chargeback if you’re unable to use a service due to travel restrictions such as border closures or not being allowed to board a flight because you have COVID-19 symptoms.

Visa also says if a company doesn’t supply a product or service due to a government prohibition, you’re not entitled to a chargeback.

In a document about managing disputes through COVID-19, Visa says an airline cancelling a flight because the government closed the border, or a gym closing because of a government mandate to stop operating, are examples of cases when you can’t get a chargeback.

But Mastercard holders do have chargeback rights when a company cancels a service – flights or accommodation, for example – due to government restrictions.

We’ve also heard from several people who’ve managed to get chargebacks for cancelled travel plans.

Jenny Krapez used a Coles credit card to pay for a holiday through an overseas travel company. When the company cancelled the trip due to COVID-19 and refused to give her a refund, Jenny asked Coles Financial Services for a chargeback.

It took several months and a lot of chasing up and required the patience of a saint or two

Jenny Krapez, Coles credit card user

She eventually got her money back through Coles, although it “took several months and a lot of chasing up and required the patience of a saint or two,” she says.

Enrica Brazzelli found herself in a similar situation when her flights were cancelled due to border closures. Her travel agency had agreed to a refund but failed to give her one.

She asked the Bank of Queensland for a chargeback on her Visa card and eventually got one, after a five-month process.

What to watch out for

Getting a chargeback can, at times, be a relatively smooth process. Greg Ross, for example, has received chargebacks three times after transactions he didn’t recognise appeared on his credit card. Greg says his bank, NAB, promptly reversed the transactions each time.

‘Don’t wait for statements to arrive’

“I track my accounts through online banking, and don’t wait for statements to arrive,” he says. That may be a wise choice, considering card schemes have time limits for disputing transactions and, if you miss the deadline, you might not get your money back.

Consumer legal centres say people tend to miss out on chargebacks because the rules and processes surrounding them aren’t transparent enough. This leads to lapsed time limits and confusion over whether banks have handled a request fairly.

“The whole chargeback system is relatively opaque for customers,” says Gerard Brody, CEO at the Consumer Action Law Centre. “Banks and card schemes should be much more clear with customers about what their rights are and when a chargeback will be provided.”

Time limits

If there’s a problem with your purchase and you can’t get a suitable remedy from the retailer, ask your bank or credit union for a chargeback as soon as possible so they can lodge it within the card scheme’s time limits.

The time frame depends on the reason you’re asking for a chargeback, but, in general, Visa cardholders have 120 days from the transaction date.

Banks and card schemes should be much more clear with customers about what their rights are and when a chargeback will be provided

Gerard Brody

For goods not supplied, Visa’s document on managing disputes through COVID-19 says cardholders have 120 days from the transaction date or from the last date you expected to receive the item to lodge a chargeback claim, as long it’s within 540 days of the transaction.

Mastercard’s deadlines to raise a chargeback for cardholder disputes and fraud are 120 days from when the transaction clears, and 90 days for authorisation issues or point-of-sale errors. The time frame can be extended to 540 days for some disputes.

Misleading claims

In April and May, the Commonwealth Bank sent letters falsely claiming they were “unable to dispute transactions that relate to COVID-19” to customers whose chargeback requests they rejected.

After the Consumer Action Law Centre lodged a complaint with the bank and ASIC, pointing out that the statement was false and misleading, the bank removed it from their letters.

“What I don’t know is how many other people saw that letter or a similar letter and didn’t pursue their rights because they were told that they couldn’t,” Brody says.

Rules that are ‘impossible to fulfil’

To customers who request a chargeback because an item they bought is not as described, the Commonwealth Bank sends a different letter.

The letter says the bank requires an “independent assessment from a licensed expert, written on their business letterhead” that explains “the difference between what you were promised and what you actually received (required by industry rules)”.

Alison Maynard, who got one of these letters after she asked the bank for a chargeback in August, says the requirement is “impossible to fulfil”.

Alison asked So Happy for a full refund, but the retailer agreed to pay only 80% of her money back

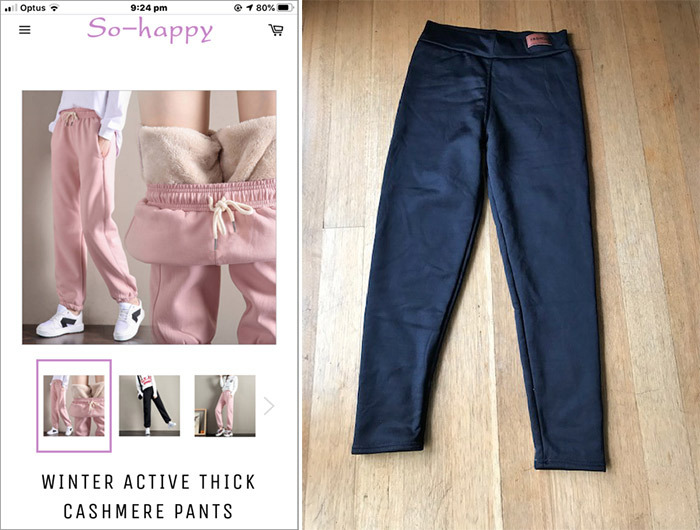

She had paid a total of $68.58 for a pair of tracksuit pants, including shipping, from online retailer So Happy. The pants she received were completely different from the ones promoted on So Happy’s website.

The pictures online showed loose-fitting pants that tied at the waist and had pockets and elastic hems. The pants that arrived in the post had none of these features. But they did have an added quirk: one pant leg was longer than the other.

Alison asked So Happy for a full refund, but the retailer agreed to pay only 80% of her money back. They then credited $26.85 into Alison’s account – less than 40% of the amount she had paid.

Alison sent the CBA pictures of the pants that were advertised (left) and the pants she received (right). The bank told her they also needed an expert’s assessment explaining the difference.

When Alison asked the Commonwealth Bank for a chargeback on her Visa credit card, they sent her the letter saying they needed an “independent assessment from a licensed expert”.

Alison searched online for a licensed valuer specialising in clothing and called one that showed up in the results. “I said I wanted a chargeback and they said they get lots of calls about this,” she says. “So I’m not the only one.”

Complicated by lockdown

The valuer said they would need to physically examine an item to value it. This wasn’t possible for Alison: the state of Victoria, where she lives, was in lockdown due to COVID-19.

Alison sent the bank her receipts, pictures of the pants that were advertised and the pants she received. She also sent copies of her correspondence with So Happy, showing that the retailer had agreed to a refund amount they didn’t provide.

She asked if she still needed to get an independent assessment, writing: “Victoria is in lockdown, and I am not sure what sort of expert would be available for this type of dispute. Surely the photos speak for themselves”.

The bank begged to differ. “Unfortunately, as you have not supplied all the requested documentation set out in our original letter, we have no reversal rights under Visa Scheme rules and have therefore closed the above reference case,” they wrote in an email to Alison.

If your bank or credit union hasn’t met their chargeback obligations, AFCA can order them to pay you compensation

But Visa tell us they don’t require an independent assessment from a licensed expert to get a chargeback. They wouldn’t comment on whether the bank had acted appropriately in Alison’s case.

Mastercard, on the other hand, may require supporting documentation from an expert in some cases where an item is defective or not as described. You don’t have to provide this when you first ask for a chargeback, but you may have to later in the dispute process.

‘Bizarre dispute’

We asked the Commonwealth Bank if they could explain the discrepancy between what they and Visa say are Visa’s rules. The bank emailed us a statement saying they “request all relevant documentation” when a customer asks for a chargeback.

“At times this may include an independent assessment to verify the goods received do not match what was promised,” the statement continues. It goes on to say the bank has reviewed Alison’s case and decided to approve the chargeback.

For Alison, the whole process has been a perplexing one. “It’s the most bizarre dispute I’ve ever been involved in,” she says.

Problem with your bank’s response?

If you believe a bank or credit union has rejected your chargeback request incorrectly, you can lodge a complaint with the Australian Financial Complaints Authority (AFCA).

According to their website, AFCA will then assess whether your bank or credit union made reasonable efforts to pursue your chargeback request.

If you believe a bank or credit union has rejected your chargeback request incorrectly, you can lodge a complaint with AFCA

This assessment includes looking at whether your bank or credit union raised a chargeback for the most appropriate reason, and that they reviewed the retailer’s response to the chargeback to determine if it was adequate.

If the dispute wasn’t resolved between your bank and the retailer’s bank, and the card scheme made the decision, AFCA can’t review whether your card scheme made the right call.

But they can review whether your bank or credit union took appropriate steps to pursue a chargeback on your behalf.

If your bank or credit union hasn’t met their obligations, AFCA can order them to pay you the refund amount or another amount as compensation.

For more than 60 years, CHOICE has been fighting the good fight for Australian consumers.

In the past year alone we've uncovered systemic issues with sunscreens, investigated shonky supermarket pricing, fought for stronger scam protections and helped make complex energy pricing fairer and clearer.

CHOICE is here to provide unbiased advice and independent testing in our world-class labs. We buy the products we test, just like you do, and our expert reviews are influence free. We’re here to help you choose smarter. Hopefully you’ll also save some money along the way.

Thanks to CHOICE, you’ll never be alone when a business treats you unfairly. You can support our work by joining or donating to our cause.