Travel insurance is an essential part of planning a holiday, but who wants to study insurance small print when you could be poring over maps and goading jealous friends with travel brochures?

This guide to getting the right travel insurance will have you back in holiday mode in no time.

In the helpful case studies you’ll find throughout this guide, we’ve changed some names and details to protect privacy.

Why get travel insurance?

If you’re an Australian travelling overseas, travel insurance is just as essential as a passport. If you can afford a holiday, you can afford travel insurance.

Holidays don’t always go as planned

Travel insurance can give you financial and practical support when things go wrong. Medical expenses are the number one risk you want to cover.

Other things that can go wrong include trip cancellations, delays, lost luggage or even natural disasters and pandemics. If you end up out of pocket because of these things, insurance could make up for your losses. But most importantly, it’s about being a smart traveller in case the unexpected happens.

The Australian government won’t pay your medical bills

If you end up injured or sick while overseas, the Australian government can only help so much. The Consular Services Charter describes what the government may do and also what it can’t do to help Australians overseas.

74% of travellers expected assistance in circumstances when the government may not be able to provide it, such as coordinate and pay for medical evacuation or treatment

ICA & DFAT Travel Insurance Survey 2025

If you end up injured or sick while overseas, the Australian government can only help so much.

With the correct travel insurance, you’ll be financially covered when things go wrong. Without insurance or the right insurance? You might need to pay for unplanned hospital bills and the cost of flying home. If you’re really unlucky, bills could cost you or your family hundreds of thousands of dollars. See the case studies highlighted in the sections below for things to check for when buying travel insurance.

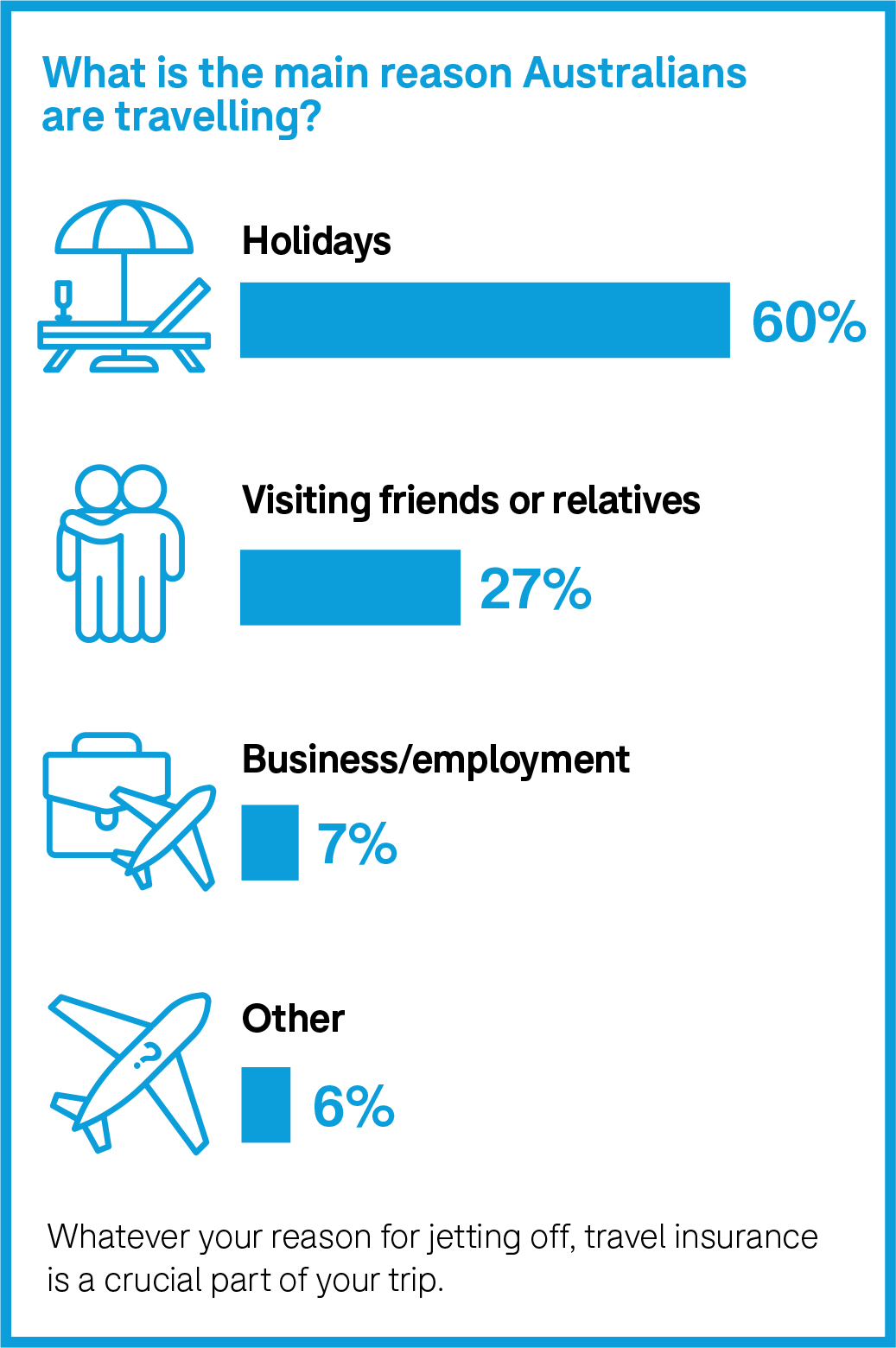

Whatever your reason for jetting off, travel insurance is a crucial part of your trip.

Travel insurance for countries with reciprocal healthcare arrangements

Australia has reciprocal healthcare agreements with several countries: Belgium, Finland, Italy, Malta, the Netherlands, New Zealand, Norway, the Republic of Ireland, Slovenia, Sweden and the United Kingdom. If you have Medicare, you can get subsidised treatment for essential services only in these countries. This often makes people wonder if they still need travel insurance?

The answer is yes, for the following reasons:

You’re usually only covered for urgent care that can’t wait until you get home.

If you’re very ill, travel insurance can pay for a medical escort to bring you home to Australia – reciprocal healthcare agreements don’t cover this.

You still might have to pay fees for treatment and medication. For example, in New Zealand reciprocal health care doesn’t cover you for free or subsidised care by a general practitioner or ambulance.

To get to most of these destinations, you often need to transit through other countries where Australia has no reciprocal healthcare agreement. And you could get injured or sick on the way.

Travel insurance also covers you for other unexpected events, including flight cancellations, delays, stolen items and more.

Remember to take your Medicare card overseas with you. You’ll need it, along with your passport, to prove you’re eligible for reciprocal health care. For more information, visit servicesaustralia.gov.au.

Tip! Did you know that some overseas hospitals won’t admit or treat you without travel insurance and that you’ll have to pay up front?

Case study: Nhung was holidaying in Türkiye when she experienced acute appendicitis and needed emergency surgery. The hospital wouldn’t admit her without payment. Nhung contacted her travel insurer and after a quick assessment of her condition, she was provided with funds so she was not left out-of-pocket and could focus on recovering.

Why travel insurance is so important

I’m travelling in Australia; do I need domestic travel insurance?

For Australians, most of us already have medical cover at home, such as Medicare, private health insurance or both. We know how things work here and we’re closer to our family, friends and support systems if we need them. But there are still a few key reasons to consider domestic travel insurance.

Medical evacuation: If your health insurance policy doesn’t cover air or ground ambulance, domestic travel insurance might be worth thinking about for emergency evacuation. For example, you go on a hike and get hurt.

Trip cancellation: If you’ve spent a lot on your holiday, then it’s not too much extra to buy travel insurance in case things go wrong.

Baggage cover: If you’re travelling with valuables, think about whether you want them covered for theft, loss or damage.

Car hire insurance excess: You can save money using travel insurance to cover your collision damage excess, instead of paying the car hire company’s extra charge.

You can buy travel insurance from a travel insurer, travel agent, insurance broker, credit card provider, or even from your health, home or car insurer.

How to buy?

You can buy travel insurance online – direct from the insurer’s website, from a comparison site or through an airline booking site – over the counter or over the phone.

When to buy?

The best time to buy travel insurance is as soon as you know your travel dates and when you book and pay for the trip. This means you’re covered if your trip is cancelled or if you’re unable to travel, even before you set foot on a plane, train or ship.

But don’t fret if you didn’t buy travel insurance at the time you booked and paid for your trip. Just make sure you buy travel insurance before your departure date. It’s better than not buying it at all. And if you’ve already set off on your travels, some insurers will let you buy a policy after you’ve already departed Australia, but with conditions.

Case study: Lewis booked and paid for a holiday in Bali through an airline. During the booking process, the airline offered optional extras such as preferred seats, meals, and travel insurance. Lewis chose to purchase travel insurance. Later, he contacted the airline to reschedule his holiday for a month later. While on holiday, Lewis became unwell and had to see a doctor. He only discovered afterwards that he didn’t have insurance coverage. His policy had expired because it covered only his original travel dates, not the rescheduled ones. When Lewis changed his travel dates with the airline, he also needed to notify the insurer. No matter how you purchase your travel insurance, be sure to understand your coverage and inform your insurer if your plans change.

What to buy?

So, you’re being a smart traveller and buying insurance. And you can certainly buy travel insurance quicker than it takes you to read this guide, but do you know what you’ll be covered for? Will you be covered if you injure yourself after having a few drinks? If you crash your scooter in Thailand? If you lose your wallet during a stopover? If you miss a flight because of a car accident?

93% of people who travelled with insurance were unaware or unsure of at least one common policy exclusion

ICA & DFAT Travel Insurance Survey 2024

There are a lot of “what ifs” to consider, depending on where you’re going and what you’ll be doing. It’s worth reading the product disclosure statement (PDS) first to make sure you’ll be covered.

Case study: Nikos and his family from Melbourne were visiting extended family in Greece during a planned three-week holiday. Midway through the trip, Nikos’ father, a Greek national who lives locally, became seriously ill and was admitted to hospital. Nikos and his family needed to stay in Greece to support Nikos’ father while doctors assessed his condition. They couldn’t return home as planned. Fortunately, their insurance policy’s trip interruption benefits covered the illness of a close relative or someone they were staying with. Nikos’ insurer covered $4500 in flight change costs. The family could arrange return flights once Nikos’ father was well enough. Under most insurance policies, the insurance period is automatically extended if an insured event prevents you from completing your trip. So the family’s coverage was extended at no cost, allowing them to stay longer without buying extra insurance.

Hopefully not, but here are the most common claimed events:

Flight or tour cancelled

Flight delayed more than 12 hours

Missed a connecting flight

Received medical treatment

Lost, damaged or stolen luggage

Lost, damaged or stolen cash or personal items

Forced to cancel trip before departure.

Will the insurers pay out?

Did you know that Australian travellers lodged over 310,000 insurance claims in 2023–24. Over 206,000 claims were accepted, paying out almost $559 million.

Top reasons for declined claims

Due to policy exclusions, or not included in the policy conditions

Claim amount was below the excess

Claim was due to a pre-existing medical condition

Claim was for an item that was stolen while it was unattended

It’s important to understand what your travel insurance will cover. Every trip and destination is different. Every traveller is different. So, if one traveller is 18 going bungee jumping and another is 81 going on a cruise, it makes sense their insurance needs are different, too.

Travel insurance with cancellation options can cover your expenses to cancel due to:

sickness or injury

natural disasters

family emergencies and

other unexpected circumstances.

You should notify your insurer immediately when cancellation becomes necessary. If you’re covered, your insurer will guide you through trying to recoup costs from travel providers like airlines and accommodation first and then cover what’s left over.

If you’re leaving Australia, travel insurance is just as essential as a passport.

Before you buy

1. Where are you going?

Travel insurance prices and coverage depend on where you travel. Some policies cover only certain countries or regions, while others are worldwide. Insurers may see some destinations or regions as riskier than others.

Not all policies cover pandemics like COVID-19 or SARS, or travel changes caused by riots or civil unrest.

Check your destination on the Smartraveller website. Make sure you’re aware of any risks and safety advice.

DFAT’s Smartraveller website assigns each destination an official advice level of 1, 2, 3 or 4. For each level, DFAT provides advice to help Australians avoid or reduce the risks to their safety. A higher travel advice level means higher risk.

It’s important to read and understand the advice level for each country you’re travelling to or through. Why? The advice level can affect your safety and your travel insurance.

Based on the Insurance Council of Australia 2025 survey, travellers weren’t always put off by travel advisories, with many unaware that they may be left uninsured if they do choose to travel.

Almost half (47%) of all travellers reported they were not aware that travel insurance policies likely wouldn’t cover their travel to a destination with a level 4 travel advisory in place

ICA & DFAT Travel Insurance Survey 2025

Tip!

Buy a policy that covers you for every country you’re travelling to or transiting through. If you’re going to Europe via a one-night stopover in the US, then check you’re covered for the US and Europe.

Most single-trip policies will cover you for 24 to 72 hours for a stopover in a country different to the region you selected when buying the policy.

Check the details of the insurance policy you’re planning to buy, to understand how long you have.

You might need different insurance cover for different regions. If you’re unsure, ask your insurer.

Insurers sometimes apply policies to regions rather than having a policy for each destination. The following is a list of regions and examples of destinations that may fall under these:

Asia Pacific: Destinations such as New Zealand, Bali, Fiji and Papua New Guinea.

Asia: Destinations such as India, Indonesia, Thailand, Singapore and Malaysia.

Europe: Destinations such as the United Kingdom, Ireland and Western Europe.

Worldwide: All the regions listed from items 1 to 3, as well as regions such as North America, South America, Japan and Africa.

Regions differ for each insurer. For example, several insurers cover travel to Bali under their Asia Pacific policy, while some will only cover travel to Bali under their Asian region policy.

2. How long are you going for?

Just a quick trip? Buy a standalone travel insurance policy for a set number of days.

Travel often? Consider an annual multi-trip policy or a credit card with complimentary travel insurance, but make sure it gives you the cover you need.

Tip! Annual multi-trip policies and credit card policies can restrict the length of each trip you take – anywhere from 15 to 365 days, depending on your policy. Some allow you to pay for extra days.

3. What are you going to do at your destination?

Cruising the open road on a scooter? Carving up the ski slopes? These things aren’t necessarily included in a travel insurance policy. It’s surprising, yes! But now you know. Different adventures, itinerary and travel styles affect your travel insurance. The more extreme your adventures, the more extreme travel insurance you’ll likely need!

Look through the insurer’s list of included activities. Check what activities you might have to pay to get extra coverage for.

If you’re planning to drink alcohol and operate a vehicle, check your travel insurance policy about alcohol limits. Why? If you’re intoxicated and you cause or are involved in an accident, your insurance policy might not cover you.

It’s no different from how drinking affects your blood alcohol concentration levels in Australia, and its legal impacts if you’re involved in an accident. If you’re overseas, similar rules apply.

4. Are you taking any valuable items?

Do you need cover for an expensive digital camera, tablet or laptop? Cover limits for such valuables can vary from a few hundred dollars to thousands. The higher cover will often mean a higher insurance premium.

Tip! Consider adding insurance cover for portable valuables to your home insurance policy instead. Remember to check on the insurance excess and if the policy will cover you worldwide and not just in Australia.

Insurance policies also vary when it comes to how they cover valuable items.

Valuables in your check-in luggage often aren’t covered.

Cover for baggage stored in your hire car is inconsistent.

Baggage left unattended is never covered. This can include a bag stolen from the seat beside you in a restaurant.

It can get a little confusing! But now you know what to check in your insurance policy.

Tip! Just like if you’re in Australia and paying for your home insurance goods, make sure you have receipts for your valuables kept in a safe place. Travel insurance won’t pay if you can’t prove you own them.

If you have a medical condition that existed before you bought your policy, it may not be covered. This can range from something as common as allergies or asthma through to diabetes, heart conditions or knee replacements.

If you’re unsure, contact the insurer to ask whether they’ll cover your condition automatically or whether they require you to do a medical assessment.

Case study: Sarah has well-managed type 2 diabetes. Before purchasing travel insurance, Sarah confirmed with her insurer that they would cover her condition. While travelling through Vietnam, Sarah experienced gastrointestinal illness due to unfamiliar food. This illness caused her blood sugar levels to become unstable, triggering complications related to her diabetes. She was admitted to hospital for monitoring and treatment for three days. Sarah’s insurance policy covered $7300 in hospital and medical costs, and additional accommodation and booking change costs for the portion of her trip she missed while hospitalised.

Case study: The Massoud family was holidaying in Singapore when 13-year-old Nazreen had a recurrence of severe bronchitis, which had affected her in Australia before their trip. The family’s travel insurer wasn’t liable to pay any hospital bills as Nazreen’s bronchitis was a preexisting medical condition. The Massoud family had to borrow $17,000 from their friends to cover Nazreen’s hospital expenses, additional accommodation and the cost of changing flights.

So, you’ve done your research and found the policy you need. You’re about to click “buy”. Then you see that checkbox you need to tick that says, “I acknowledge I’ve read the product disclosure statement”.

But wait… before you tick it, have you actually read the product disclosure statement (or PDS)? In the insurance world, that “fine print” is the product, and it pays to know what product you’re buying.

How to read the PDS

There are hundreds of policies out there. If you tried to read all the paperwork and the PDS that comes with each policy, you’d have to extend your holiday just to recover.

Tip! If you don’t have time to read the whole PDS, at least look for the following:

Table of benefits gives you an overall summary of your cover.

Policy cover section is essential reading. It’s generally split into “what we will pay for” and “what we won’t pay for”.

General exclusions section is essential reading. These are events that aren’t covered by any section of your policy.

Pre-existing conditions can remind you of forgotten ailments. It’s essential reading for anyone with any kind of medical condition, no matter how mild.

Word definition table might contain a few surprises. It’s a good place to check on the definition of a ‘relative’ or a ‘scooter’, for example.

Claims section lists some more pointers to be aware of. For example, most insurance policies state that you must not admit any liability in an accident without their consent. Also remember to keep any paperwork, such as police reports, that you might need to make a claim.

24-hour emergency assistance contact number – write it down and keep it handy.

The list of travel insurance disputes taken to the Australian Financial Complaints Authority (AFCA) shows many cases of unread or misinterpreted policy terms and conditions. Between 1 July 2024 and 30 June 2025, AFCA received 2036 travel insurance complaints.

Not all travel insurance policies are the same. The wrong policy can be almost as bad as none.

Tip! Contact AFCA if you feel your declined claim wasn’t right.

Case study: Katherine’s luggage was stolen from the designated cargo section onboard a bus in Barcelona. The insurer declined her claim for €2500 in losses (over $4000). According to the insurer, Katherine should have had the bag on her lap or stood beside the bag in the cargo section of the bus, instead of leaving it “unattended”. AFCA ruled in Katherine’s favour, saying it “was not reasonably possible for the complainant to avoid leaving her bag unattended in the circumstances”. The insurer was to accept and pay the claim for Katherine’s lost luggage in accordance with the policy terms.

This is the number one reason to buy travel insurance. Look for the insurer’s benefits table. If you’re searching online, the benefits table is usually on the ‘Quotes’ screen. If you’re looking at the PDS, it’s near the beginning of the document. The PDS gives a quick overview of what the insurer is offering. Most policies have an ‘unlimited’ sum insured.

Pre-existing conditions

Some insurers don’t cover pre-existing conditions at all. Some will only cover pre-existing conditions with an extra fee and sometimes a medical assessment. Some automatically cover pre-existing conditions listed in their PDS, but few will cover mental illnesses such as depression or anxiety.

Most insurers don’t cover certain pre-existing medical conditions and generally don’t provide cover for any illnesses or incidents that arise from these. This includes terminal illness, or any illness that shortens your life expectancy.

Minor pre-existing medical conditions such as asthma, hypertension, diabetes, epilepsy, osteopenia and more are usually covered if:

the condition has been stable for more than 12 months

there is no planned surgery

you have not received treatment in the past 12 months.

Could a pre-existing condition spoil your holiday plans?

findaninsurer.com.au lists insurers that might provide cover for pre-existing conditions.

Still having trouble finding cover? Get help from an insurance broker.

Examples of conditions that usually need you to be assessed before getting cover are:

coronary problems

lung disease

epilepsy

stroke or

any surgeries in the last two years.

If in doubt, declare your condition to your insurer at the time of purchase. Ask questions to make sure you understand what you are or aren’t going to be covered for. Then you can make an informed decision.

Disability cover

A disability shouldn’t prevent you from buying travel insurance, but it might make finding a good policy trickier and more expensive.

Is a disability a pre-existing condition?

It depends on the disability and the insurer. Many insurers will automatically cover travellers with limited mobility, cognitive impairments or vision/hearing impairments. But in some cases, this cover may come at an extra cost.

Check with the insurer as some conditions are assessed on a case-by-case basis.

Having trouble getting cover?

Under the Disability Discrimination Act 1992, insurers must assess the actual risks, rather than make assumptions about disabilities. If you’re having trouble getting insurance, a letter from a medical professional might help. Especially if the medical professional can state that you’re not likely to need medical or hospital treatment while on your trip.

Cover for your equipment

If you’re travelling with a wheelchair, mobility aid or hearing aid, you’ll need to insure that as well. Check single item limits, which are usually between $750 and $1000 per item. If you have a piece of medical equipment that exceeds this, you’ll need to specify it and insure it separately.

Items like artificial limbs and hearing aids may be subject to separate limits, so check the fine print and take out extra insurance if necessary.

Cover for your carer

If you’re travelling with a carer, it’s a good idea to be on the same policy in case travel plans change for either of you – that way you’re both covered. If you have a paid carer, ask your insurer whether they’ll cover the cost of a replacement carer, in case yours can’t travel.

Are you covered for pregnancy complications? Some insurers don’t cover pregnancy at all.

Up until which stage of pregnancy? Pregnancy complications are usually only covered up until a certain stage (often between 23 and 32 weeks, depending on the insurer).

Childbirth: Not all insurers will cover childbirth. A premature birth in the United States (US) with intensive care and treatment could end up costing hundreds of thousands of dollars.

IVF: Not all insurers will cover in vitro fertilisation (IVF) pregnancies.

Do you have to pay extra to be covered for pregnancy? Some insurers may require you to pay extra for pregnancy to be covered.

Do you need a letter from a medical professional to say you’re fit to travel? Insurers may also require you to obtain medical approval before covering you.

Tip! Travel insurance generally covers only the people named on the policy. If you’re travelling while pregnant, ensure your policy covers all pregnancy stages and associated costs for your new baby, before and when they arrive.

Case study: Emma and her partner visited Japan for a short babymoon. Emma was 22 weeks pregnant when they travelled, so before buying her policy, she checked the insurer’s pregnancy cover. It covered pregnancy complications up to 24 weeks. During the trip, Emma experienced unexpected pregnancy-related complications and was advised by a local doctor to rest and undergo monitoring. She was admitted overnight for observation and follow-up care. As her pregnancy was within the policy’s covered gestation period and there were no known complications prior to travel, the policy responded. Emma’s insurer covered medical consultations, diagnostic testing, hospital costs and additional accommodation expenses, while Emma recovered before being cleared to continue her journey.

Mental health cover

Travel insurers will generally cover medical expenses for mental health conditions experienced for the first time on the trip but cover for existing mental health conditions can be trickier.

Insurers may provide cover if you declare mental illness as a pre-existing condition and pay a higher premium. Check the PDS carefully. Insurers may use different terms to describe the same mental health conditions so be sure ask your insurer is something isn’t clear.

Declare your pre-existing condition as insurers are highly unlikely to pay a mental health-related claim you didn’t declare. An insurer might view a single visit to a therapist many years ago because of work stress, for example, as a pre-existing mental health condition.

Mental health and travel insurance have been a contentious issue for consumer rights groups including CHOICE. And it’s one that’s still evolving from a legal standpoint.

To find out if a travel insurance product includes mental health cover, review the cover at choice.com.au/travelinsurance, and then carefully review the PDS.

Age restrictions

Most policies have an age limit, ranging right up to the 100-year-old seasoned adventurer. There are quite a few conditions for older travellers including:

Higher premiums: Insurers often charge older travellers more, and in some cases ‘older’ can be as young as 50.

Higher excess: Travellers as young as 60 but more commonly over 80 could be subject to a higher excess because of their age. The normal excess of around $100 to $200 is often increased to an excess of $2000 to $3000 for travellers 80 years and over for claims that relate to injury or illness.

Restricted conditions: ‘Subject to medical assessment’, ‘reduced medical cover limits’, ‘reduced travel time’, ‘policy to be purchased 6 months in advance’ – all these conditions can apply to travellers over a certain age.

Case study: Bethany was travelling with family when their flight from Amsterdam to London was delayed. The delay caused them to miss their connecting flight from London to Melbourne. As the connecting flight was booked with a separate airline, they were not provided with any accommodation and had to incur out-of-pocket costs for an additional flight home. Their travel insurance policy provided limited cover for a situation where scheduled transport that was cancelled or delayed caused you to miss a connecting flight (provided you allow a reasonable time between connections). So the insurer covered their accommodation and travel costs in London, because it was the initial delay that caused them to miss their connecting flight.

Cancellation cover

Plans can sometimes change. Your travel plans are no exception to this rule. You may have to cancel your trip because of illness, the airline might cancel the flight on you, or something outside of everyone’s control, like a pandemic, can change everyone’s plans.

Travel agents and third-party booking sites like Booking.com, Expedia and Airbnb all have their own terms and conditions. They are the first port of call to determine whether you’re eligible for a refund or credit. But the fine print is still subject to Australian Consumer Law.

So what are your rights and how can you get your money back?

You’ll probably want to be covered if your travel plans are cancelled for any reason. Be aware that in some circumstances insurers won’t pay for cancelled trips. Check the kinds of cancellations and conditions you might not be covered for.

Examples may include:

Terrorism: Most insurers cover medical expenses but very few cover cancellation expenses in the event of terrorism.

Pandemic or epidemic: Commonly excluded.

Military action: Actions such as war, civil war, rebellion or insurrection are commonly excluded.

Natural disaster: Covered more often than not, but worth checking as some policies exclude cover for this situation.

Cancellation that is the travel provider’s fault: Insurers commonly exclude cover for delays or rescheduling caused by the transport provider.

Just as there are common exclusions to cancellation payments, travel insurance can still cover you for cancellations, delays, stolen items and more if you have the right policy.

Whether you can get your money back from an airline, travel agent or booking site for changed or cancelled travel plans usually comes down to whether it’s you or the airline or travel provider who is making the changes.

You’re more likely (but not always) eligible for a refund or credit if a travel provider, such as an airline, cruise line or hotel, has cancelled the service you were due to receive.

If you cancel the trip or change your plans, it may be deemed a ‘change of mind’ and your options for a refund or credit may be reduced.

Tip! You’ve invested in travel policy. So, invest time to ensure you know what kind of transport interruptions and cancellation you’re covered for.

Almost two-thirds (62%) of overseas travellers who buy insurance do so on or before the day of booking travel

ICA & DFAT Travel Insurance Survey 2022

What are ‘unforeseen circumstances’?

When an insurer refers to cover for ‘unforeseen circumstances’, it means something that wasn’t publicised in the media or official government websites when you bought the policy. Check the Smartraveller travel advicewhen you buy your travel insurance.

If a circumstance, risk or event is known before you buy the policy, you won’t be covered if it directly affects your travel. The earlier you buy travel insurance, the more likely you are to be covered if something unexpected happens at your destination before your trip.

For example, imagine you buy travel insurance three months before your trip. Two weeks before you’re due to travel, a natural disaster hits your destination and all flights are cancelled.

Because you already bought travel insurance, you should be covered and able to claim your money back. But if you didn’t buy travel insurance before the disaster happened, you usually won’t be covered for any losses, even if you bought the travel insurance before you left Australia.

Tip! Buying travel insurance earlier than your departure date might cost a little more, but it also might save you a lot more if the unexpected happens.

Case study: A week after a volcanic eruption made world news, Sameer booked a trip to Bali. He assumed the emergency would be over by the time he was due to fly a month later. Unfortunately, the volcano continued to erupt, and Sameer’s flight was cancelled. His insurer declined his claim because he’d bought the flight and insurance after Smartraveller issued a travel alert about the volcanic eruption, and after it had been in the news.

Travel insurance and Smartraveller advice

The Smartraveller website, which the DFAT manages, assigns an overall advice level to more than 175 destinations. This advice level can affect your travel insurance cover.

Travel warnings can work in your favour. If an insurer excludes cover for a known event, they may still cover you to change your plans in response to updated advice from Smartraveller.

For example, most travel insurers cover natural disaster as long as you bought the policy before it became a ‘known event’. Cover will vary between policies. CHOICE did a comparison on a variety of international travel insurance policies. Most covered medical expenses in a natural disaster.

But in a natural disaster you’re more likely to need cover for cancellation expenses, for example if you’re unable to get to the airport due to bushfire, your flight is cancelled or delayed because of a volcano erupting, or you’re stuck in transit.

Travel insurance may cover you for:

Your medical expenses due to natural disaster

Cancellation if the area where you are travelling is affected and your accommodation is closed, the area is unsafe, the government has closed roads or asked people not to travel or to leave.

Travel delay if you can’t get to your flight or transport, either internationally or domestically.

Emergency expenses, for example if your trip is disrupted by volcanic ash cloud.

There are several insurers that may not cover cancellation or other expenses in these situations, so make sure you check with your insurer and the policies they offer.

But beware when travelling to a destination that has a ‘Do not travel’ warning as most standard policies won’t cover you.

If you are travelling to, or transiting through, a ‘Do not travel’ or ‘Reconsider your need to travel’ destination, look for a provider that specialises in high-risk, complex environments or war-zone travel insurance and carefully check the policies they offer. It is critical to have the right coverage for high-risk destinations as the Australian Government is usually extremely limited in its ability to help you in these locations.

Delays can be expensive, particularly if you have to pay for alternate transport or accommodation. These extra expenses won’t always be covered.

Transport delay is only covered after a certain number of hours, usually six, but you might have to wait as long as 12 hours before your cover kicks in.

Cover limits for transport delays are typically lower than other cover limits and are often limited per 24-hour period.

Insurers often exclude cover for rescheduling caused by the transport provider. But some may cover additional accommodation and travel expenses in this scenario for travellers who are en route.

For example, if you’re prevented from travelling due to unexpected circumstances, some airlines will provide you with a credit for future travel (possibly after deducting a fee). It depends on whether the delay or cancellation was due to something within the airline’s control.

If you think your trip won’t proceed, or you’re worried about travelling due to illness or Smartraveller destination alerts, speak to your airline, booking site and/or travel agent about your options.

Baggage cover

Baggage cover varies widely, from $0 to $25,000. So, if you’re not carrying expensive items, you might be able to save on your premium by selecting a policy that provides lower coverage.

Individual items are subject to sub-limits that range from around $200 to as much as $6000.

Higher item limits usually apply for electronic items like laptops, cameras, smartphones and tablets.

You can pay extra to specify items you want extra cover for (insurers are always happy for you to pay extra).

Valuables locked in a car or checked in on an airline, train or bus may not be covered.

Generally, any items left unattended may be excluded from cover, so keep your belongings close.

Case study: While sightseeing in Barcelona, Daniel was pickpocketed in a crowded area. His mobile phone and wallet were stolen. Despite reporting the incident to local police, the items could not be recovered. Since Daniel promptly reported the theft to police, and was able to prove ownership of his phone, the insurance policy covered the value of the stolen phone, the cost of the wallet, and replacement costs for essential documents, including his driver’s licence.

Lost luggage

If an airline loses your luggage temporarily and doesn’t compensate you for that loss, you may be able to claim expenses for clothing, toiletries and other necessities, depending on your policy.

Cover usually only applies to luggage lost for more than 12 hours, though the minimum time limit varies per insurer, as does the level of cover.

If your policy has an excess (a fee that’s deductible from your payout), remember that this applies once per claimed event, and items below the excess level can’t be claimed.

Case study: Kim and her partner were travelling through Europe when severe weather caused widespread transport disruption. Their scheduled service was cancelled, which resulted in them missing their onward flight home. With no alternative flights available that day, they incurred additional accommodation, meal and transport expenses while waiting for replacement flights. After returning to Australia, Kim lodged a claim with her insurer, providing receipts and confirmation of the disruption. Her insurer assessed the claim and reimbursed the reasonable additional expenses incurred as a direct result of the delay, in line with the policy terms.

Car hire cover

Car hire companies offer insurance, for an additional cost, that reduces the amount of excess you’ll have to pay in the case of an accident. Alternatively, you could use the collision damage excess cover in your travel insurance. It will still be subject to the terms of your rental contract, so you’ll still need to check the car hire company’s terms and conditions, but it may save you the extra insurance cost.

Tip! If you use your travel insurance in place of the rental company’s insurance, you’ll need to pay out of pocket to the rental car company first, and then claim a reimbursement from your travel insurer.

Do you have the right licence?

Some countries require you to have an international driving permit or a permit issued by that country. If you have an accident while driving on the wrong licence (or breaking that country’s law in any other way), you may not be covered.

Cruise ships carry a higher risk for spreading disease compared to other non-essential activities and transport modes. COVID-19, influenza and other infectious diseases such as gastroenteritis spread easily between people living and socialising in close quarters.

Check travel insurance policies to make sure medical cover for contagious diseases such a pandemic or influenza is included, as some policies exclude this cover.

Case study: Erica stumbled and broke her leg during stormy seas while on a cruise. Her insurer covered the cost of evacuation and a partial hip replacement at a hospital in Noumea. It also organised and paid for her son to fly to Noumea to help Erica recover and return home to Australia. Five months later, the well-travelled 82-year-old was boarding a plane to Croatia for her next fully insured adventure.

Cruising but not leaving Australian waters?

You still need insurance. Doctors working on cruise ships don’t need Medicare provider numbers to provide medical care. If they treat you, you can’t claim on Medicare or your private health insurance, even if you’re still in Australian waters.

Domestic travel insurance doesn’t cover medical costs, so you need either international travel insurance (check that it covers domestic cruises) or a domestic cruise policy.

Case study: Margaret travelled on a multi-night cruise, departing and returning to Sydney, with no stops in other ports. Despite not leaving Australia, the onboard medical services were privately provided and not covered by Medicare, as is often the case with domestic cruises. Margaret bought a travel insurance policy that covered domestic cruises. During the cruise, Margaret became unwell and required medical treatment on board the ship. She was required to pay for treatment at the time. But Margaret was covered by her insurer, who reimbursed the cost of her onboard medical treatment in accordance with the policy terms.

Adventure activities cover

When CHOICE compares travel insurers we look at who covers which sports and adventure activities, such as skiing, ballooning, bungee jumping and scuba diving.

But as always with insurance, the PDS can include some surprises. For example, several insurers we’ve reviewed will cover canyoning, but they won’t cover abseiling, often a necessity in canyoning. Other policies in our comparison will cover abseiling, but not into a canyon.

If you’re planning on doing anything adventurous, check to make sure you’re covered. It’s not enough to simply look for the tick next to your chosen activity – you also need to check the definitions in the PDS.

Motorcycles and scooters

Hiring a motorcycle or scooter? Depending on which country you’re in, you might need a local or international motorcycle licence. You probably won’t be covered if you aren’t obeying the local law. And even if you are doing the right thing under local law, some policies still won’t cover you unless you have an Australian motorcycle licence, even if the country you’re in doesn’t require you to hold one.

Are you wearing a helmet? Most countries say you need one by law, but that doesn’t mean it will be included in your hire. No helmet means no cover (in more ways than one).

Case study: Liam was holidaying in Bali and hired a scooter to travel short distances. Before riding, he confirmed the engine size and ensured he held the appropriate Australian licence for the type of vehicle he was hiring. During his trip, Liam was involved in a low-speed accident and required medical treatment. Liam’s medical expenses were covered by his insurer because he was correctly licensed to ride that type of vehicle under Australian law, complied with local laws (including wearing a helmet), and met the policy conditions relating to motorised vehicle use.

Skiing and snowboarding

Some insurers cover skiing, often for an extra premium. Not so many insurers cover skiing ‘off-piste’, away from the groomed runs. If you’re tempted to slide off the beaten path next time you hit the slopes, make sure you have a policy that covers off-piste ski runs (or pay for the optional extra cover).

Otherwise, if you have the wrong insurance, ski into a tree and have to be evacuated from the mountains, it could cost you thousands of dollars.

It’s worth remembering that travel insurance only covers overseas costs. So, if you break a leg while you’re abroad, your insurer will likely pay your hospital fees, but they won’t cover your ongoing physiotherapy once you’re back home.

Case study: Marianna fractured her leg in three places while skiing with her partner and children in Japan. Because the family had bought additional cover for winter sports, they were reimbursed $35,500. This paid for medical expenses, additional transport and accommodation, the cost of a nanny to look after the children, and business class flights back to Australia.

Alcohol and drugs

31% of insured travellers didn’t know their policy’s alcohol limits.

ICA & DFAT Travel Insurance Survey 2025

Overdoing it on vodka and float-tubing down a river isn’t likely to be covered by any policy. Insurers won’t pay for costs arising from you being under the influence of alcohol or drugs, except where taken under the advice of a doctor.

Even one or two drinks could be enough of an excuse for insurers to get out of paying. Some insurers specify a blood alcohol limit, but many don’t. If they think the amount you’ve had to drink caused or contributed to the event you’re claiming, they might try to deny the claim.

Look for the alcohol or liquor clause under the General Exclusions in the fine print.

Many policies cover the costs to travel home if one of your relatives dies or becomes sick. Keep in mind:

an insurer’s definition of a ‘relative’ may differ from yours

cover is usually dependent on the age of that relative, so the death of your 84-year-old grandma may not be covered

your relatives are subject to the same pre-existing condition exclusions as you, so if your 84-year-old grandma died from a known heart condition, you may not be covered.

you may be able to apply for your relative’s pre-existing condition to be assessed before you buy the policy.

cover is limited to relatives who live in Australia, or in some cases New Zealand. So, if your 84-year-old grandma doesn’t live in Australia or New Zealand, you won’t be covered to fly there for her funeral.

Case study: Michael had to cancel his trip when his father in Spain suddenly died. The insurance policy covered expenses to cancel a trip and return home to a sick relative. The policy only covered this if the relative lived in Australia. Michael’s claim for cancellation expenses was declined.

Does international travel insurance cover pandemics?

Many travel insurers offer limited cover for pandemics, but the available cover varies quite a lot. Most, but not all, policies cover medical costs for a pandemic disease. But these policies might not cover you to cancel your trip because of a pandemic.

Safeguard your travel plans

The COVID-19 pandemic showed that travel plans can change for reasons entirely outside your control. What should you do if your travel plans are interrupted at short notice? Travel insurance might not protect you from government border closures, general lockdowns or quarantine requirements in your destination country. The key is to understand what travel providers like airlines and cruise ships offer if things change.

Check the rules for travelling to your destination. For example, are there any entry requirements? What are the vaccination requirements? And what type of travel insurance do you need?

Read the terms and conditions of your airline, accommodation and travel tours before you book. Will they refund you if you can’t travel due to a pandemic? If they only offer a reschedule or a credit, will you be able to redeem the credit in future?

Keep on top of the latest travel advice and requirements at smartraveller.gov.au. Travel restrictions can change at short notice.

Travel agents and provider insolvency

What if you’ve booked and paid for your holiday through a travel agent, but then the travel agent goes bankrupt? You’ll get your money back, right? Not necessarily.

Only a few insurers will cover you for the insolvency of a travel provider. This includes hotels, airlines and other transport companies that might go bankrupt overnight. But there are a few ways to safeguard your hard-earned holiday.

Check your PDS or ask your insurer if they cover you for insolvency.

Check with your travel agent if they have insolvency insurance. Insolvency insurance isn’t compulsory, so only some agents will have it.

Pay with your credit card. Some banks allow a ‘chargeback’ if you pay for something on your credit card and don’t end up getting it. A chargeback is when you ask the bank to reverse a transaction on your card that you dispute.

Tip! Don’t accept any dodgy contract terms that require you to give up your chargeback rights.

Only one quarter of policies in the CHOICE travel insurance comparison cover insolvency

Credit card travel insurance

Some credit cards come with complimentary travel insurance. They’ll cover you for all the usual things like medical emergencies, cancellation and protection for baggage and items. But they do differ from standalone policies, so it’s essential you check the fine print.

Fees: You’ll pay a premium for these credit cards, usually between $100 and $450 per year.

Excess: The excess on credit card policies tends to be fixed at a higher rate (usually around $250). Excess rates on standalone policies are more variable.

Age limits: Some credit card policies have no age limit, which can be handy for older travellers.

Regions: Credit card travel insurance is not based on location, which means you can travel from Europe to the US without having to worry if your policy covers both areas. Keep in mind that travel to some countries such as Cuba, Iran or North Korea may be excluded.

Baggage cover: Credit card insurance often offers higher coverage for baggage loss and damage.

Trip duration: Credit card insurance policies vary in how many days of coverage they’ll give you per trip – anywhere from a few weeks to 365 days – so check your limit if you’re going on a long holiday.

Pre-existing conditions: Chances are your credit card insurance won’t automatically cover your pre-existing condition. You’ll need to call your insurer and see if you need to pay an extra fee or premium.

Domestic travel: Credit card insurance doesn’t apply to domestic travel. Some cards will reimburse expenses associated with domestic flight delays and missed connections to international flights.

Making a claim: You may not be able to claim reimbursement unless you pay for purchases – such as emergency items after a baggage delay – with the same credit card.

Is it activated?

Credit card insurance usually activates when you buy your air tickets (or sometimes other transport or accommodation expenses) using your card.

Policies require a minimum spend to activate – usually around $500. So, if you bought your tickets on sale for $499, you won’t be covered.

If you want cover for your spouse or dependants, you must also buy their tickets on your card.

Some policies only activate if you book a return ticket. A one-way flight, or even two one-way flights, will leave you uninsured.

Some banks require you to notify them to get full coverage for each trip. While base coverage will still give you emergency medical treatment, you might not get coverage for property damage or luggage delays. Check whether you need to do anything to activate any extra features.

Some cards will cover you if you use rewards points to buy your tickets. Others won’t.

Case study: David booked a trip to North America for himself and his family, including his 11-year-old daughter Petra. The trip was cancelled because Petra got pneumonia. Unfortunately, David only activated his credit card travel insurance about an hour before the family was scheduled to fly out of Australia. The travel insurer denied his claim for cancellation costs because he knew about his daughter’s illness when he activated the policy.

Is a credit card’s free travel insurance worth it?

If you already have a credit card and use it regularly, the free comprehensive travel insurance on your card can save you money. And if you’re a regular traveller without a credit card, it’s worth considering. Especially if you travel at least once a year or every second year internationally.

Jodi Bird is the Managing Financial Content Editor at CHOICE. Previously at CHOICE, he worked as Travel project lead and as a Finance specialist.

Jodi has extensive experience in financial services, having worked with major banks such as CBA, Westpac and Credit Suisse. He enjoys breaking down complex consumer decisions into easy to understand steps and holding companies to account for failing their customers. He is regularly called upon for expert commentary by major broadcasters such as the ABC, SBS, and Channels 7, 9, and 10.

Jodi has a Bachelor of Commerce majoring in Economics from the University of Wollongong. He is RG146 compliance certified to provide general advice for General Insurance and is a Responsible Manager on CHOICE's Australian Financial Services License. LinkedIn

Jodi Bird is the Managing Financial Content Editor at CHOICE. Previously at CHOICE, he worked as Travel project lead and as a Finance specialist.

Jodi has extensive experience in financial services, having worked with major banks such as CBA, Westpac and Credit Suisse. He enjoys breaking down complex consumer decisions into easy to understand steps and holding companies to account for failing their customers. He is regularly called upon for expert commentary by major broadcasters such as the ABC, SBS, and Channels 7, 9, and 10.

Jodi has a Bachelor of Commerce majoring in Economics from the University of Wollongong. He is RG146 compliance certified to provide general advice for General Insurance and is a Responsible Manager on CHOICE's Australian Financial Services License. LinkedIn

For more than 60 years, CHOICE has been fighting the good fight for Australian consumers.

In the past year alone we've uncovered systemic issues with sunscreens, investigated shonky supermarket pricing, fought for stronger scam protections and helped make complex energy pricing fairer and clearer.

CHOICE is here to provide unbiased advice and independent testing in our world-class labs. We buy the products we test, just like you do, and our expert reviews are influence free. We’re here to help you choose smarter. Hopefully you’ll also save some money along the way.

Thanks to CHOICE, you’ll never be alone when a business treats you unfairly. You can support our work by joining or donating to our cause.